How to Read Labels From a Credit Card Processors Statement

Advertiser Disclosure: Our unbiased reviews and content are supported in part by chapter partnerships, and we adhere to strict guidelines to preserve editorial integrity.

"It's 11 o'clock. Do you know where your children are?"

This was a popular PSA broadcasted to parents in the '70s and '80s, back when "stranger danger" was simply about the scariest affair out there. Now, I accept an equally important PSA for small concern owners: "You take your processing argument. Exercise yous know your pricing model?"

The ability to recognize merchant account pricing models (and, about importantly, which one yous have) is a crucial pace toward understanding your statement, every bit well as increasing your overall merchant-savvy.We've found that many merchants recognize the rates and fees they were quoted for processing, just without any broader context of which pricing model they have. This makes deciphering an already-confusing carte processing statement all the more hard, and makes discerning whether you're paying too much virtually impossible.

Starting with a argument and working backward to an authentic understanding of how your quoted rates actually kicking in is possibly non the ideal introduction to pricing models. Even so, this is most often the way things go, and I'chiliad not surprised. No 1 goes to "merchant account school" for this stuff, and business relationship providers vary widely in both their skill and willingness to thoroughly explain pricing.

The good news is that small business owners are no strangers to learning on the wing. And so, take hold of a statement or two, and let's become cracking!

A Quick Primer On Pricing

In broad strokes, the main pricing models are differentiated by the style your merchant business relationship provider handles the wholesale cost of processing (what it must pay to other entities in the processing chain) versus its ain markup. At that place are ii separate types of wholesale costs — interchange fees and card clan fees — merely the differences between pricing models generally center around how interchange fees are handled.

You're probably already aware of the vast variety of credit and debit cards in circulation. Each type of card has its own pre-set interchange cost (a per centum of the sale and sometimes a per-transaction fee) that all merchant account providers must pay to the menu-issuing bank when that particular card blazon is used. Over the years, the main merchant business relationship pricing models have developed based on two possible ways of dealing with these wholesale interchange costs:

- Pass the interchange costs straight to the merchant and as well charge a separate "low" markup.

- Blend the interchange costs into one or more than "high" overall rates for the merchant that alreadyinclude a markup.

I'grand putting "depression" and "high" in quotation marks considering we recognize they're super-relative terms. Not to mention, the exact amount of your rate is only i piece of the puzzle. As a helpful simplification going frontward, you can recollect of "low" as well nether 1%, and high as over 1% (often at least 2%, or even much more). The important thing to remember is that a low rate may not include interchange already (expect for those costs listed separately), while a high rate likely does.

The "Large Iv" Models

The most common pricing models are interchange-plus, membership, flat-rate, and tiered. For more background on the models, check out these helpful articles:

- Trading Ease For Transparency With Interchange-Plus

- Tiered Pricing: The Epic Fail Of A Pricing Model

- Get A 0% Interchange-Plus Markup With Membership Fee Pricing

- Analyzing The Price-Effectiveness of Square's Mobile Processing Solution (apartment-charge per unit pricing)

If you're yet a fleck foggy on the differences, that's okay. For now, you can start with your statement and work toward a better understanding of merchant business relationship pricing as a whole. We'll get there!

Good Indicators, But Non Guarantees

While each pricing model leaves tell-tale signs on a statement, it's important to note that no "standard" indicator is necessarily a guarantee. Remember of the indicators we'll hash out as good clues, or of import signs. In truth, processors may include red herrings in their statements, or invent their ain strange hybrid systems. Fortunately, virtually stick fairly closely to the main pricing models.

Now, nosotros're finally ready to look at the four primary pricing models and their near common statement indicators. The more indicators for a certain model on your statement, the better the odds that'south the model you take. I'll exist using a few snippets of statements as examples, but note that any interchange rates listed are not necessarily the current values. Some of the statements are older. In any instance, your statement will never match these completely. No two processors display this stuff in the same mode.

Interchange-Plus / Toll-Plus Pricing

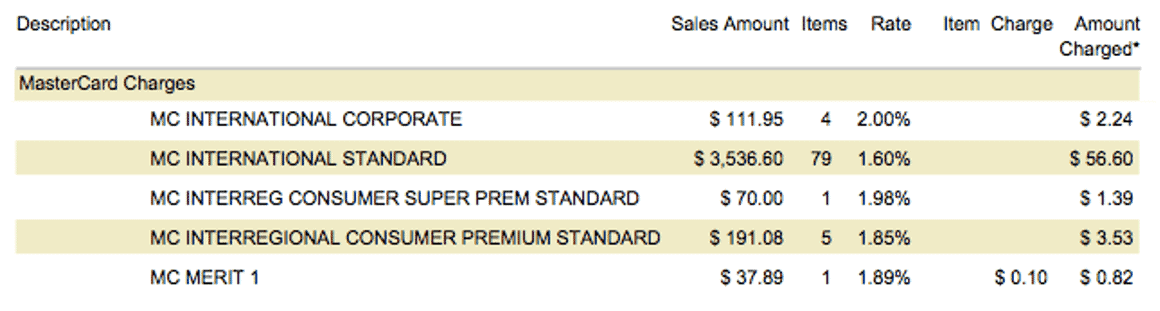

All things being equal, interchange-plus statements are the almost hard to read. The big payoff is that yous clearly encounter the difference between wholesale costs and your account provider's markup on your statements. In this model, the charge per unit you lot were quoted was just the markup piece — the "plus" in "interchange-plus." In other words, interchange fees and your account provider's markup are charged separately. Typically, interchange-plus plans charge both a percentage markup and a flat, per-transaction markup. Here'southward what you'll likely see on your statement:

- Itemized Interchange Rates:

Example A: 1 pocket-sized section of a long list of interchange rates. Notation that each type of menu is charged its own pre-set rate, and passed through to the merchant.

- Consistent "Low" Pct Markup:Charged separately from interchange fees.

Example B: Consistent markup of 0.40% listed after each bill of fare type's itemized listing of interchange fees. All transactions/card types have the same 0.xl% markup.

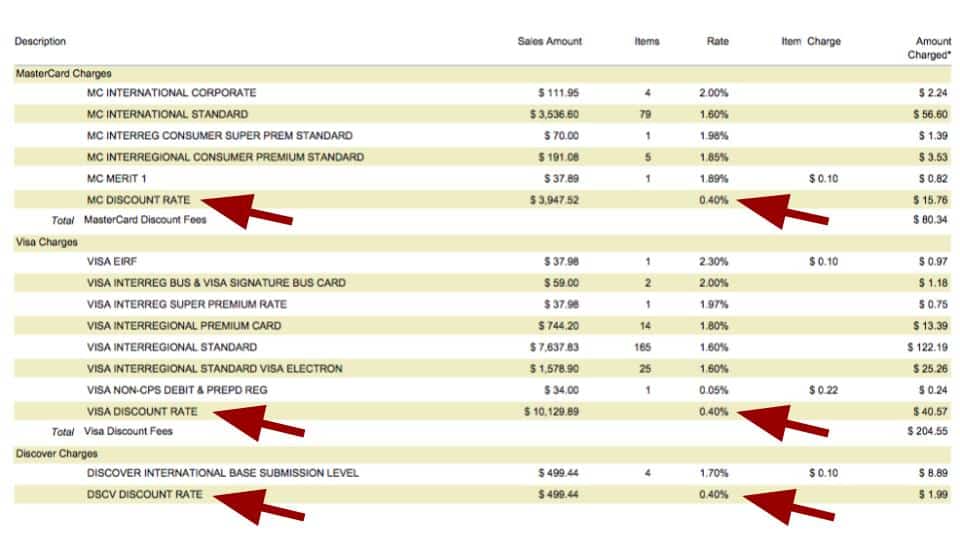

Instance C: In the "Rate" column, a consistent 0.31% markup is shown directly above the itemized interchange rate for each type of menu/transaction.

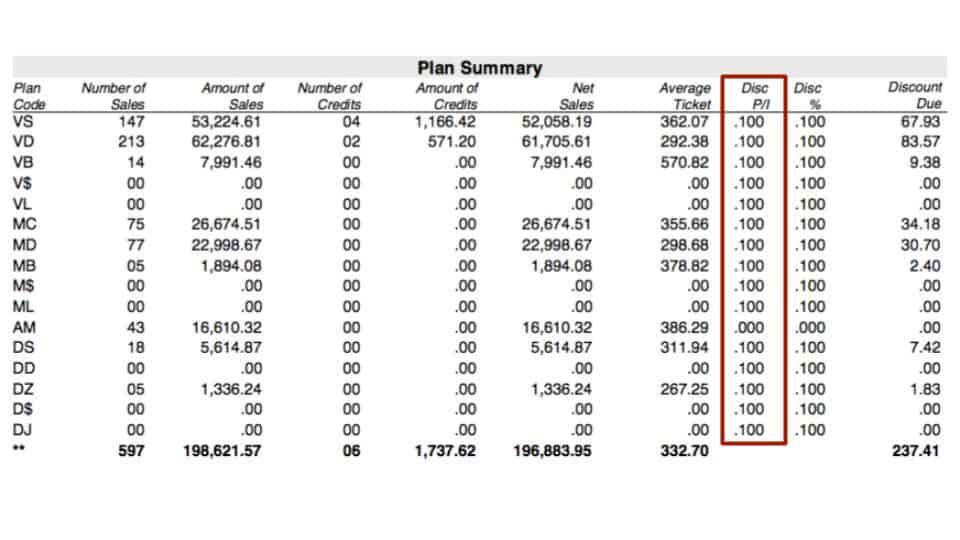

- Consistent Transaction Fee Markup: This per-transaction markup may be found in the same line items every bit the per centum markups, or downwardly in a separate "authorization" section.

Instance D: Along with a consistent 0.10% markup across the board (Disc %), in that location's a consequent $0.10 transaction fee markup (Disc P/I) for all card/transaction types.

Subscription / Membership Pricing

Membership pricing is sort of a riff on interchange-plus. The wholesale interchange rates are still charged separately from the business relationship provider'south markup. The difference is that the markup comes in the form of one flat monthly subscription fee, and also a pocket-size, per-transaction markup. No percentage markup is charged. Here are the primary argument indicators of subscription pricing:

- Itemized Interchange Rates: Like to Case A above.

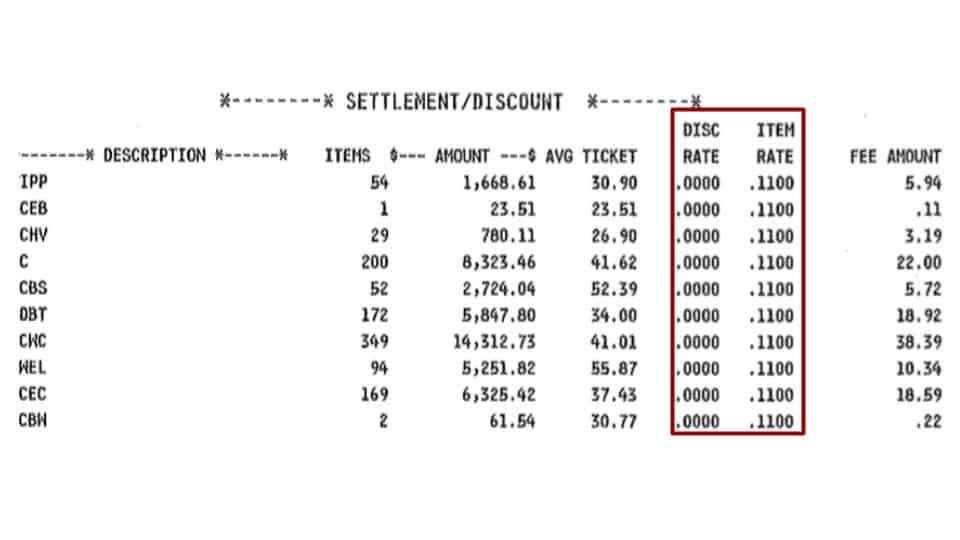

- Consistent Transaction Fee Markup:See Example E below.

- No Percentage Markup: See Example Due east beneath. Notation that percentages will still be part of itemized interchange rates (not shown below), just no separate percentage markup is present.

Example E: Consistent $0.11 "Particular Rate" charged on all card/transaction types. No "Disc Rate" % markup. This business relationship had a membership fee of $120/calendar month (not pictured). Interchange rates were itemized separately (non pictured).

Flat-Rate / Composite Pricing

This is the model most unremarkably offered by third-party payment facilitators (a.k.a. PSPs, merchant aggregators) like PayPal, Stripe, and Foursquare. Occasionally, traditional merchant business relationship providers employ it also. In this all-inclusive model, wholesale charges and the processor'due south markup are all composite together into your one, flat processing rate. If a per-transaction fee is part of your rate, this also goes toward covering your provider's wholesale costs plus any turn a profit margin. Your flat charge per unit covers all types of transactions, from inexpensive signature debit transactions, all the mode to expensive business rewards cards. You'll typically detect:

- No Itemized Interchange Rates: Your argument is quite simple, merely you tin can't come across the actual wholesale cost behind any of your transactions.

- Consistent "High" Rate: If any charge per unit is displayed at all, it's ordinarily just i main charge per unit in the high two% to mid-three% range, and sometimes you'll see a per-transaction fee as well. Note that some PSPs accuse a couple different high rates based on the type of transactions you run (i.eastward., keyed or ecommmerce vs. swiped/dipped.)

Tiered / Bundled Pricing

This is another example where y'all can't see the itemized interchange rates split from your processor's markup on your statement. Instead, your transactions are first grouped into tiers according to the processor's pre-fix criteria. Each group (tier) is then charged a flat charge per unit that already includes the interchange costs for those transactions. If you've got a tiered plan simply have but been quoted one rate, information technology'south typically the charge per unit for transactions that fall under the everyman, "qualified" tier. In reality, some transactions may be downgraded to college priced tiers (mid-qualified and non-qualified). Y'all have no real mode of predicting these downgrades ahead of fourth dimension. Here's what you'd see:

- No Itemized Interchange Rates: You mostly won't come across a listing of interchange charges–considering why list them if they're already blended into your tiered rates?

- Qualified, Mid-Qualified, Not-Qualified Labels: Whatsoever line items with whatever of these labels (or similar-looking abbreviations) is your biggest clue.

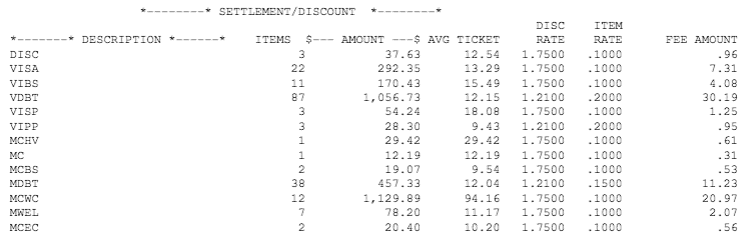

Example F: Transactions are charged one.75%, 2.75% or 3.25% depending on the tier

- Multiple Rates, Usually "Loftier": By definition, a tiered program must take at least two charge per unit levels or tiers shown on the statement. The standard model is 3 levels: qualified (lowest), mid-qualified (middle), and non-qualified (highest). Annotation that some providers may create a separate set of 3 tiers for debit transactions, because these wholesale debit costs are cheaper. The bottom levels of a signature debit tier tin really be "low" (well under 1%) and however account for the interchange cost or human action as a loss leader. Y'all'll demand to be certain that there are no other higher rates charged on your argument (and examine other indicators) before you lot can assume your "low" rate means you're on interchange-plus! On the other mitt, all credit card tiers will probable exist well over 1% and in the "high" category, so look for those every bit a better indicator. When you're looking for multiple rates on your statement, the mid and non-qualified transactions may be listed right next to the qualified ones, or may exist shown as split surcharges later in the statement (similar in Instance H below).

Case G: Two "loftier" rates are charged, 1.75% + $0.10 for credit, and ane.21% + $ 0.20 for debit. These are the two qualified tiers of this program.

Example H: In the same statement as in a higher place, we find a surcharge section. 20-ii transactions were downgraded to not-qualified (amounting to an actress 2%) and 30 to mid-qualified (an extra ane.47%). Multiple rates for multiple tiers at play!

Concluding Thoughts

Did you lot recognize your ain pricing model among these main 4 types? If you fabricated it this far with your statement, I promise you lot've at least developed a strong hunch. While each model has its merits for different situations, y'all can probably tell we adopt the inherent transparency and comparability of models that dissever out the interchange costs from the account provider'southward markup. By the same token, nosotros have a hard time getting behind the unpredictable downgrading and surcharging of tiered pricing. I'd encourage you to check out our elevation merchant account providers if you're looking for a fresh start. All of them offer transparent interchange-plus or subscription pricing plans.

Parents of the 70s and 80s feared "stranger danger" above all else, merely my biggest fearfulness for merchants is that they pay as well much or fifty-fifty go scammed considering they don't have a solid agreement of their processing statements. Knowing and recognizing your pricing model is 1 of your best protections as a merchant. If you're still unsure nigh yours, drop u.s.a. a line and we'll meet if nosotros can help!

rodriguezastat1988.blogspot.com

Source: https://www.merchantmaverick.com/how-to-identify-your-merchant-account-pricing-model-on-your-processing-statement/

0 Response to "How to Read Labels From a Credit Card Processors Statement"

Post a Comment